JHVEPhoto

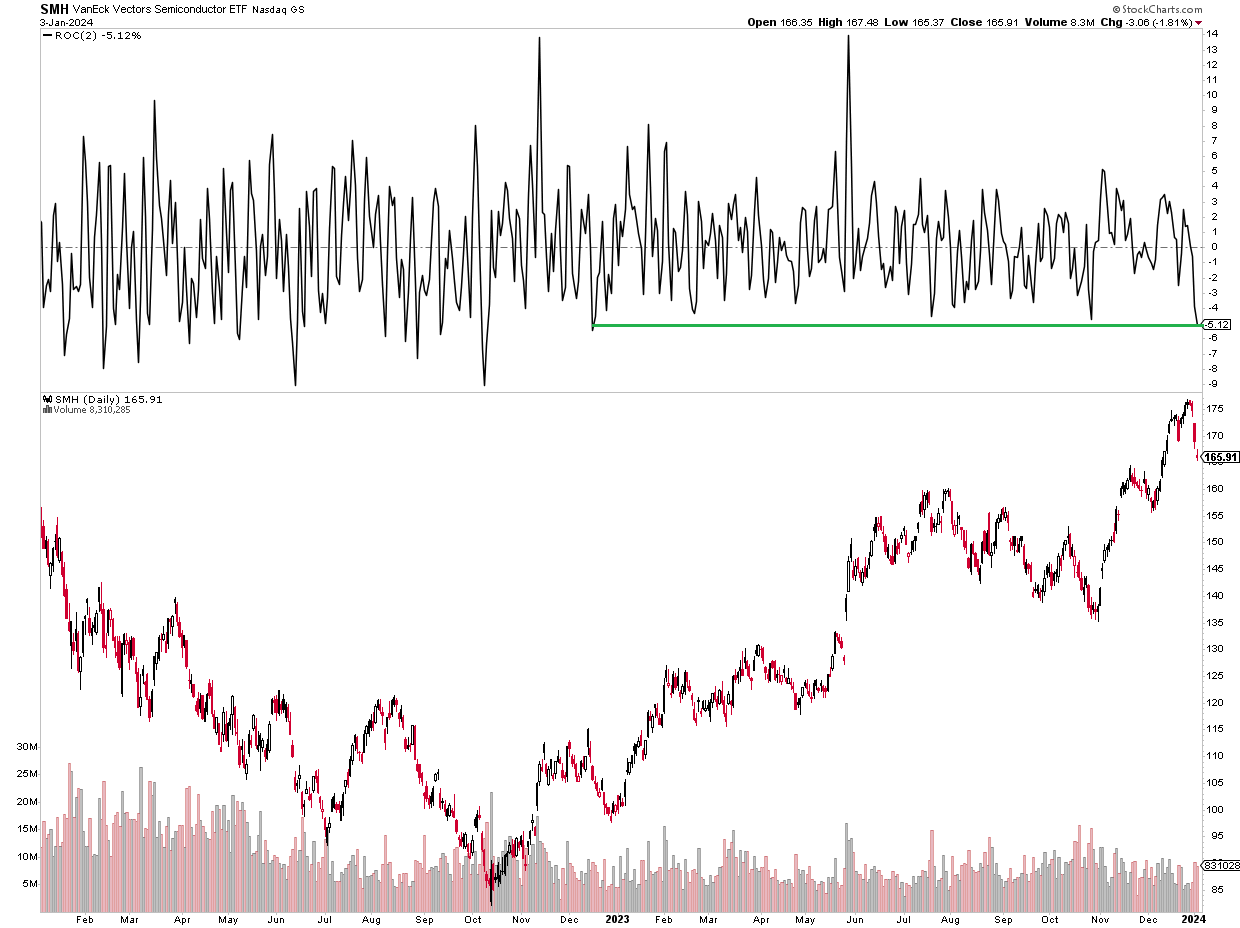

It has actually been a rough start for a few of 2023’s winners. Particularly, semiconductor stocks have actually struggled to kick-start the year. I saw that the very first 2 sessions of January were the worst back-to-back trading days considering that December 2022 for the VanEck Semiconductor ETF ( SMH). After an excellent last 12 months, a pullback may make good sense, however I continue to see essential advantage in one worldwide chip gamer.

I restate my buy score on Qualcomm ( NASDAQ: QCOM). Following another quarterly EPS beat with robust profits development ahead, I see the stock as underestimated with technical strength.

SMH Chips ETF Suffers A Considerable Dip To Start 2024: worst back-to-back sessions considering that December 2022 -5.1%

Stockcharts.com

According to Bank of America Global Research study, Qualcomm styles, establishes, and products semiconductors and gathers royalties on cordless portable gadgets and facilities based upon its dominant position in code-division numerous gain access to (CDMA) and other associated innovation patents. In addition, Qualcomm offers systems software application and parts to cordless handset suppliers and promotes applications and services that work on high-speed cordless networks. The business runs mostly through 2 sectors: CDMA Technologies and Innovation Licensing.

The San Diego-based $153 billion market cap Semiconductors market business within the Infotech sector trades at a low 14.9 forward 12-month non-GAAP price-to-earnings ratio and pays an above-market 2.3% dividend yield. Ahead of its Q1 2024 profits report due out later on this month, the stock includes a moderate 29% suggested volatility portion and has a low 1.4% brief interest since January 3, 2024.

Back in November, Qualcomm reported a strong set of Q4 outcomes. Non-GAAP EPS of $2.02 topped the Wall Street agreement outlook of $1.91 while $8.7 billion of profits, down 24% from year-ago levels, was a little beat. Fast development in Android handset need assisted the chip stock together with expenses that were typically in check throughout the quarter. That mix resulted in a healthy 31% operating margin. The management group likewise anticipates Q1 deliveries from significant Chinese handset makers to confirm at a 35% consecutive development rate. Another possible chauffeur of future profits is its chips being utilized in the next Samsung phone edition.

With full-year 2024 development in handset deliveries around 10% and maybe strong fundamental development in the external year, I continue to like the essential background for QCOM. Do not mark down the strength in the car market either– its Q4 exposed a high 23% consecutive development rate because sector, though its IoT sector was uninspired. In regards to Q1 2024 assistance, earnings are seen in the $9.1 billion to $9.9 billion variety with non-GAAP diluted EPS from $2.25 to $2.45. That’s a positive outlook in the middle of a background of a brand-new iPhone launch and anticipated need from China.

Secret dangers emerging for QCOM today consist of macro weak point in China and the possibility of continuous stress in between Apple and Huawei. Weaker worldwide smart device adoption in the middle of a slowing economy might likewise harm the company, while margin pressure because situation would be most likely. Likewise, QCOM’s penetration into the 5G competitive market has actually been remarkable, however it might produce a lofty expectations bar moving forward, so state experts at Morgan Stanley.

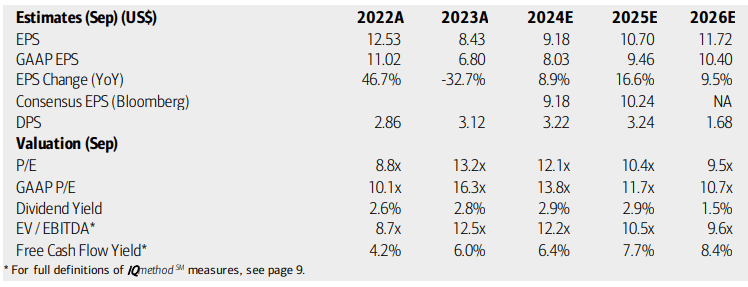

On evaluation, experts at BofA see profits increasing at a strong 9% clip this year, with a velocity in per-share revenues in 2025. An ongoing double-digit fundamental development rate is seen in 2026. The present agreement, per Looking for Alpha, reveals running EPS topping $10 next year and climbing up above $11 in 2026, all while profits development remains in the 5% to 9% variety.

Dividends, on the other hand, are anticipated to increase at a constant speed over the coming quarters. QCOM continues to be a strong totally free capital generator– the present TTM FCF yield is 6.4%. The business likewise includes an EV/EBITDA ratio that is listed below that of the S&P 500.

Qualcomm: Incomes, Assessment, Free Capital Projections

BofA Global Research Study

If we presume $9.50 of forward non-GAAP EPS and use a 17 forward running profits numerous, then the stock needs to trade near $162. That is up from my previous evaluation quote, offered lower rates of interest today and a natural increase in anticipated EPS over the coming 12 months. I continue to like Qualcomm’s capital metrics, though shares are not as appealing when examining sales multiples.

QCOM: Usually Beneficial Assessment Metrics

Looking For Alpha

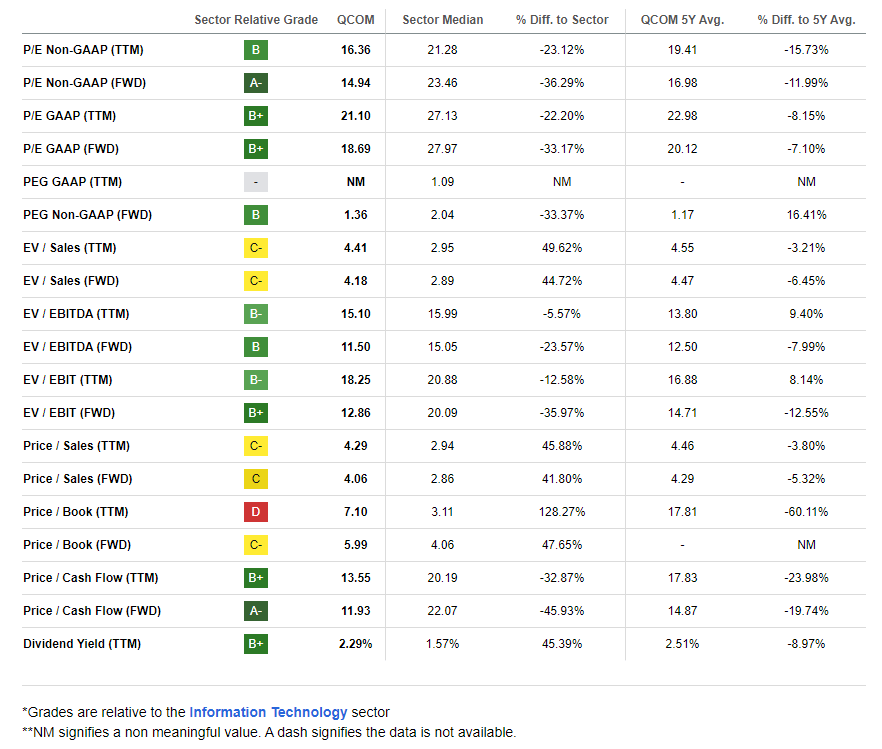

Compared to its peers, QCOM includes a near-average evaluation as the whole area experiences typically healthy chip need. Historic development has actually been weak, causing the bad grade (non-GAAP EPS fell 33% in 2023), however I assert that the development trajectory is far more sanguine. Qualcomm is amongst the most successful and greatest companies from a totally free capital point of view, while share-price momentum has actually been strong– I will information essential cost indicate enjoy on the chart later on in the post. Lastly, EPS modifications have actually been blended recently, though QCOM has actually topped profits quotes in each of the last 12 reports.

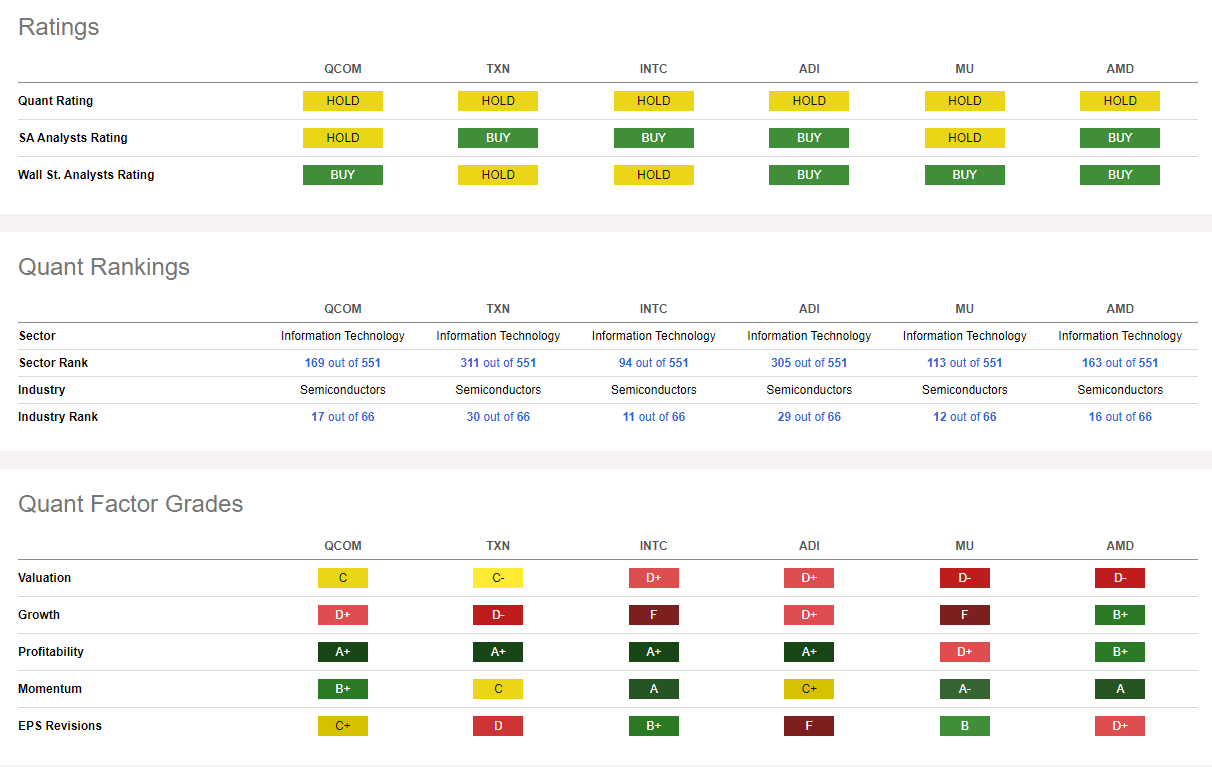

Rival Analysis

Looking For Alpha

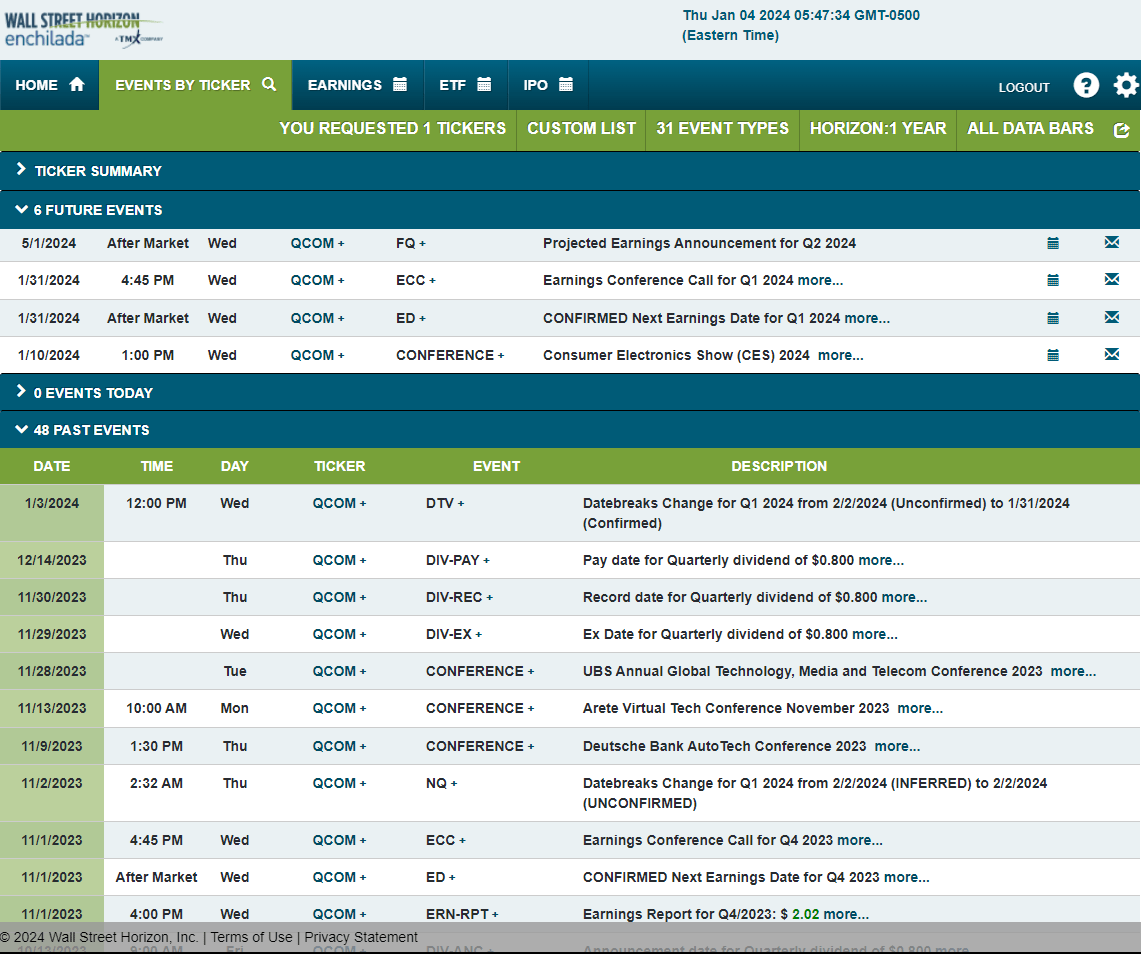

Looking ahead, business occasion information offered by Wall Street Horizon reveal a verified Q1 2024 profits date of Wednesday, January 31 AMC with a profits call right away after outcomes cross the wires. You can listen live here Before that, Qualcomm is slated to take part at the

Customer Electronic Devices Program (CES) 2024 from January 9 through 12 in Las Vegas.

Business Occasion Threat Calendar

Wall Street Horizon

The Technical Take

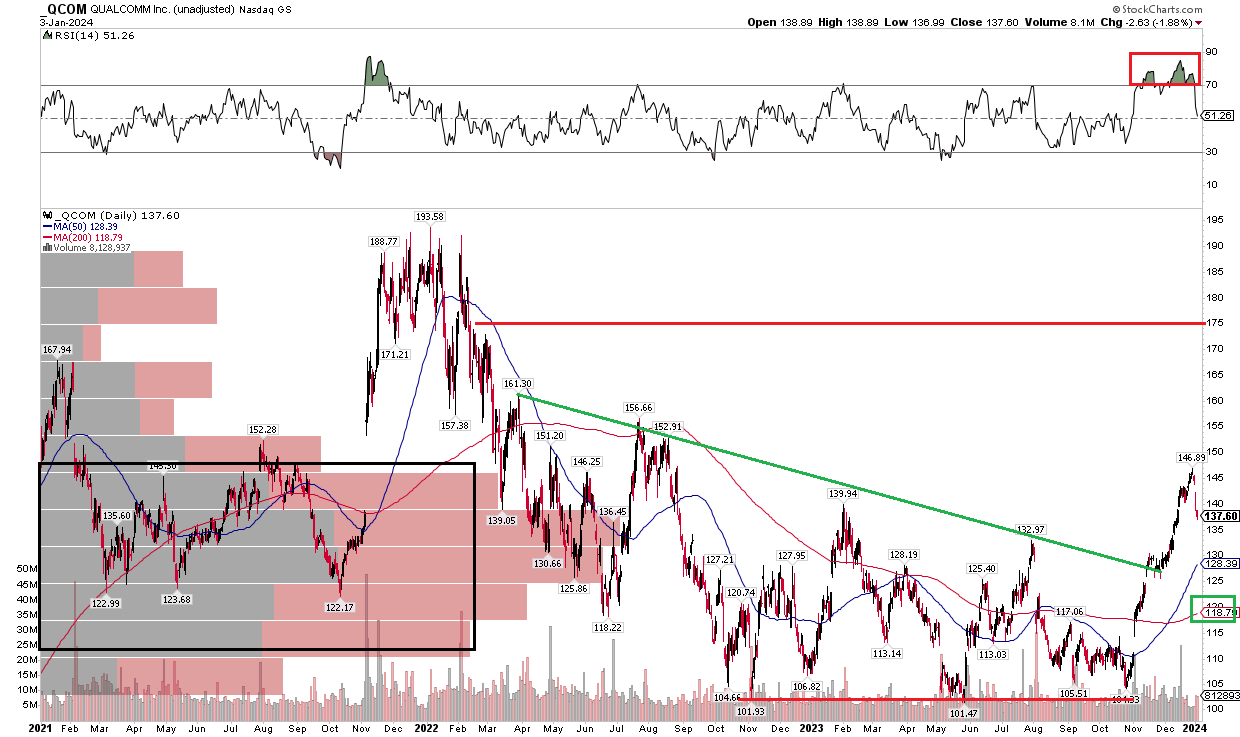

I took a long-lasting view of QCOM in my previous analysis in Q3 in 2015. Focusing, I see that the stock has actually broken out from a debt consolidation that included an essential sag resistance line. Notification in the chart listed below that shares rallied above the $130 mark throughout Q4 in 2015. The stock has actually pulled away in the middle of the early-year selloff in the tech sector, falling from $147 to $138, however with a long-lasting 200-day moving average that is now upward-sloping, the pattern appears to prefer the bulls.

I continue to see broad assistance near the $101 mark, and the coming down triangle breakout causes an upside determined relocation cost goal to near $175 based upon the height of the triangle at its beginning and after that including that height to the $130 breakout point. $175 likewise has confluence with the variety lows from the late 2021 to early 2022 highs. In the meantime, QCOM is sweating off technical overbought conditions, so purchasing on a pullback to the $130 breakout point might be a beneficial risk/reward play.

In general, I see QCOM’s chart as useful after holding essential assistance near $101 and after that rallying through resistance.

QCOM: Bullish Benefit Breakout, $175 Technical Target

Stockcharts.com

The Bottom Line

I restate my buy score on QCOM. I see shares as a strong GARP have fun with remarkable EPS development ahead and a strong technical background.