Daniel Grizelj

We formerly covered Shopify ( NYSE: STORE) in November 2023, discussing its outstanding FQ3 ’23 outcomes, with the robust customer costs adding to its broadened GMVs and GPVs.

With several e-commerce and online payment platforms still extremely durable regardless of the unsure macroeconomic outlook, it was unsurprising that the store stock had actually likewise rallied over optimistically and forward appraisals pumped up, leading to our restated Hold ranking then.

In this short article, we will go over why we are lastly re-rating the store stock as a Buy, considering that it appears that its successful development pattern and growing management in the United States e-commerce SaaS market might never ever come low-cost after all.

Integrated with the management’s appealing Free Capital assistance, our company believe that the SaaS business has actually lastly turned the corner, with very little money burn and much healthier balance sheet ahead.

We have actually Ignored store’s SaaS Financial investment Thesis – Update To A Buy

In the meantime, store has actually reported a leading/ bottom line beat in its FQ4 ’23 revenues call, with incomes of $2.14 B ( +25.1% QoQ/ +23.6% YoY) and adj EPS of $0.24 (+71.4% QoQ/ +1300% YoY).

Much of its tailwinds are associated growing Gross Product Volume of $75.1 B (+33.6% QoQ/ +23.1% YoY) and Gross Payment Volume of $45.1 B (+37.5% QoQ/ +31.8% YoY), as more merchants/ purchasers significantly embrace its payment platform at 60% (+6 points QoQ/ +4 YoY).

store’s rate walkings have actually likewise worked as meant with Membership Solutions profits broadening to $525M (+8% QoQ/ +31.1% YoY) and Month-to-month Recurring Profits to $149M (+5.6% QoQ/ +36% YoY) by the most current quarter.

The increased penetration of Shopify Payments and growing GMW have actually likewise added to its growing Merchant Solutions profits of $1.6 B (+33.3% QoQ/ +23% YoY).

As an outcome of the continual tailwinds, it is unsurprising that store has actually reported broadening gross margins of 49.5% (-3.1 points QoQ/ +3.5 YoY).

This uptrend is substantially helped by the enhanced operating costs and sale of its logistic sector, setting off the SaaS business’s favorable operating margins of 13.8% (+0.7 points QoQ/ +17.8 YoY) for the 2nd successive quarter.

The store management has actually made fantastic usage of the raised interest environment to make $272M in annualized interest earnings (+7.9% QoQ/ +71.8% YoY) in FQ4 ’23 also, naturally adding to the broadening Free Capital generation of $446M (+61.5% QoQ/ +395% YoY).

Last But Not Least, store has actually likewise used an appealing FQ1 ’24 assistance, with incomes development at “mid-to-high-twenties” on a YoY basis, gross margins of around 51% (+1.5 points QoQ/ +3.5 YoY), and Free Capital margins in the “high-single digits.”

These suggest that the SaaS business has actually lastly turned the corner, with a sustainable development pattern and no additional money burn progressing.

At the very same time, store has actually assisted “consecutive enhancement in its Free Capital generation every quarter throughout the year,” suggesting that the net money on balance sheet might continue to grow from existing levels of $4.09 B (+2.2% QoQ/ -1.9% YoY).

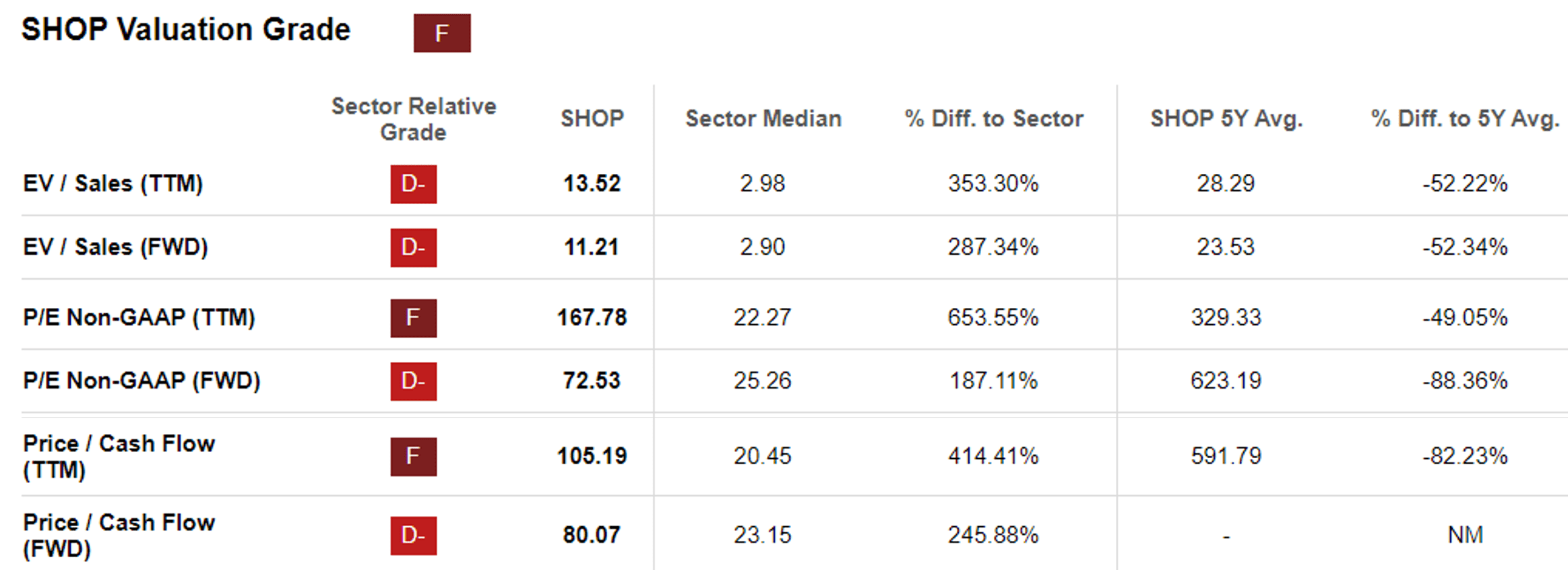

Store Appraisals

Looking For Alpha

Presuming that the store management has the ability to provide as guaranteed, we can comprehend why the marketplace has actually granted store with the premium successful development appraisals at FWD P/E of 72.53 x and FWD Cost/ Capital of 105.19 x.

While moderated from the 1Y mean of 328.87 x/ 111x, the large space compared to the sector mean of 25.26 x/ 23.15 x can not be rejected certainly.

Even if we are to compare store’s FWD P/E appraisals to other e-commerce stocks, such as Amazon ( AMZN) at 40.22 x & & MercadoLibre ( MELI) at 73.98 x, and e-commerce SaaS peers, Wix.com ( WIX) at 30.26 x & & Squarespace ( SQSP) at 41.55 x, it appears that the previous’s successful development pattern has actually been handsomely granted.

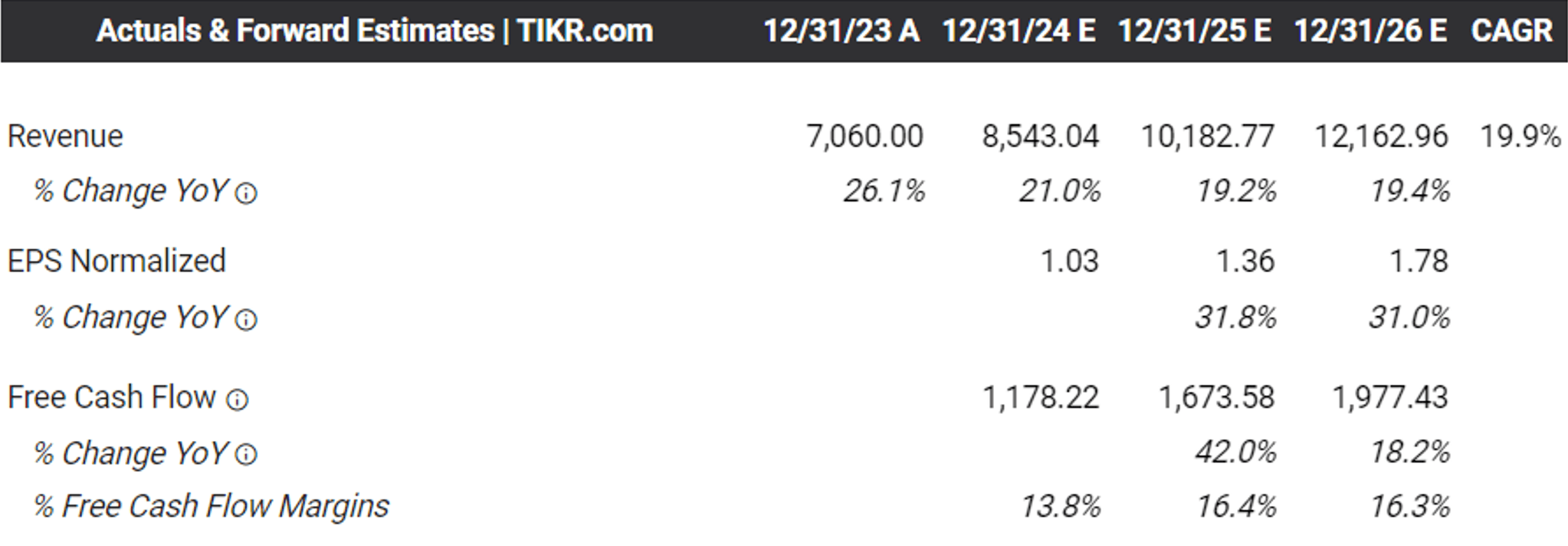

The Agreement Forward Price Quotes

Tikr Terminal

Unsurprisingly, thanks to the management’s appealing assistance, the agreement have likewise reasonably raised their forward price quotes, with store anticipated to create a broadened leading/ bottom line CAGR of +19.9%/ +57% through FY2026.

This is compared to the previous price quotes of +19.3%/ +35% and historic top-line development of +51.3% in between FY2016 and FY2023, respectively.

If anything, the international retail market size is anticipated to grow from $26.4 T in 2021 to $32.8 T in 2026 at a CAGR of +4.4%, with the retail e-commerce market size forecasted to speed up from $5.78 T in 2023 to $8.03 T in 2027, broadening at an almost doubled CAGR of +8.57%.

With store offering total omnichannel offerings in both front-end/ back-end and throughout various platform sizes/ rate points, our company believe that its potential customers are substantially helped by the robust discretionary costs and growing e-commerce sales, as likewise reported by AMZN and Costco ( EXPENSE) in current months.

Nevertheless, financiers should likewise size their portfolios appropriately, with the stock exchange currently going into severe greed levels, with any miss out on in store’s future revenues and deceleration in development most likely to set off uncomfortable corrections and downgrades ahead.

So, Is Store Stock A Purchase, Offer, or Hold?

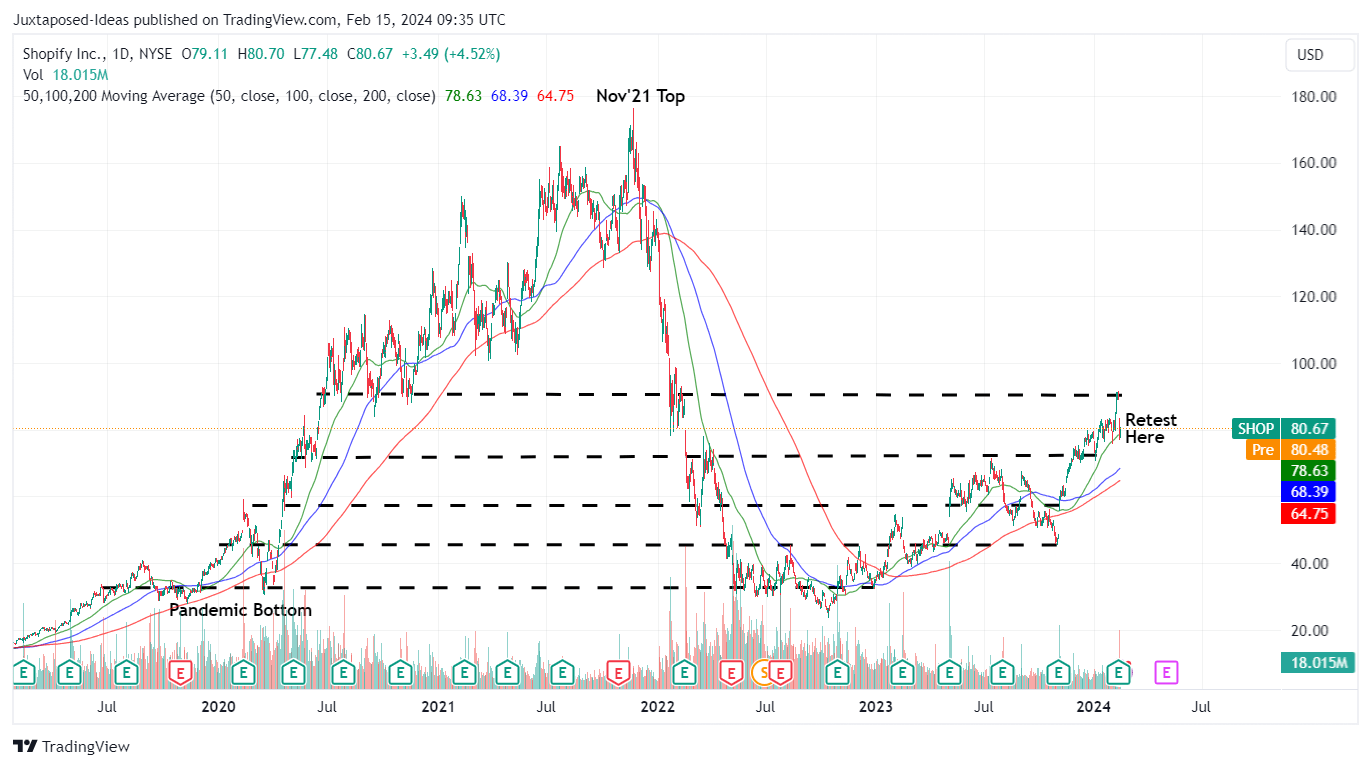

STORE 5Y Stock Cost

Trading View

In the meantime, according to a lot of tech stocks, store has actually quickly climbed up out of the October 2022 bottom while surpassing the SPY’s 1Y efficiency of +20.82% with +65.48% rally.

With the marketplace regrettably over-reacting to its apparently “ narrow FQ4 ’23 revenues beat,” the stock has actually likewise returned part of its current gains, while retesting its previous 2020 assistance levels of $80s.

In spite of the correction, store seems trading method above our reasonable worth quote of $33.30 with a significant premium of +142.2%, based upon the FWD P/E of 72.53 x and the FY2023 adj EPS of $0.46.

On the other hand, based upon the agreement FY2026 adj EPS price quotes of $1.78, there appears to be a more than outstanding upside capacity of +60% to our long-lasting rate target of $129.10. Naturally, this is presuming that the stock has the ability to sustain its premium appraisals progressing.

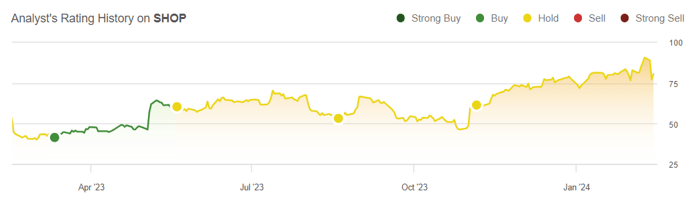

Author’s Historic Ranking For Store

Looking For Alpha

While we have yet to get on the store train, it is likewise obvious that we have actually been extremely incorrect considering that our last Buy ranking in March 2023, with us losing out on the stock’s doubling so far.

It appears that store’s management in the United States Headless Commerce SaaS market with 20.64% in market share since January 14, 2024 (+0.66 points QoQ) might never ever come low-cost after all, specifically considering that the nation’s e-commerce profits of $727.2 B in 2023 is 2nd just to China at $1.3 T.

This likewise exhibits how the management’s R&D efforts have actually prospered incredibly well in making sure the platform’s growing importance, regardless of the several rate walkings so far.

As an outcome of the appealing long-lasting threat/ benefit ratio and the extra tailwinds from the rate walking for the Plus strategies and Shopify Payments from February 2024 onwards, we are very carefully re-rating the store stock as a Buy.

Bottom fishing financiers might think about awaiting a moderate pullback, ideally at its previous trading series of in between $65 and $70s for an enhanced margin of security.

Moving on, our company believe that the store stock might gradually become premium appraisals, for so long that it continues to provide high development, broadening revenue margins, and increased market share.